The crypto world is abuzz right now with news of new insurance-based crypto wallets. The recent crypto wallet insurance options try to address the paradox of crypto and decentralized money: how should users retain control of their money while still receiving some protection or insurance in case of disaster?

Deposits today are secured up to $250,000. There is no such coverage for crypto.

Source: https://commons.wikimedia.org/w/index.php?curid=7919770

No federal FDIC insurance policy exists to protect users from loss as it does with fiat. The reality is that crypto demands a high level of personal responsibility – managing one’s own money independent of any centralized entity means that you’re entirely responsible for all scenarios. Unfortunately, things frequently go wrong. Hacks and theft compromise millions of dollars a year in crypto and the loss of private keys and backup phrases compromise millions more. In fact, it’s estimated that the total loss of bitcoin to private key mismanagement is upwards of 20% of all existing bitcoin. The risk of private key mismanagement is perhaps the single greatest barrier to wide-scale crypto adoption.

Because of this, many companies focus on providing viable protection to users. Zengo’s CEO, Ouriel Ohayon, published an article in Forbes last year discussing the importance of viable crypto-insurance options.

Several options exist for users to protect their crypto, but they all force users to trust a central entity, provide only limited protection, and necessitate high fees.

The goal of this post is to help you understand the available options for protecting your crypto. We’ll explore the different insurance-based models and investigate whether Zengo offers enough safety guarantees to adequately protect crypto holders on its own.

Types of crypto-insurance

Crypto insurance is attractive at first glance. Civic recently announced that its multi-sig wallet will be insured up to $1 million per user, much to the excitement of the industry.

.@Coincoverglobal is now providing automatic insurance cover worth $1 million for users of Civic’s cryptocurrency hot wallet.@paddybaker_ reports @civickey https://t.co/Jzaqx85pjV

— CoinDesk (@CoinDesk) March 31, 2020

But while there are many insurance options available, each has its own set of pros and cons. Read the “fine-print” carefully to see whether the policy is right for you.

A range of different insurance options exist. We’ll explore the various offerings and discuss the pros and cons of each option.

Insured Exchanges

Some users trust exchanges with their crypto storage.

Many of these exchanges choose to finance their own insurance plans. Binance allocated 10% of its total trading fees to an insurance fund and paid out $40 million from that fund during the recent Binance hack. Stable coin provider, Equilibrium, maintains a fluctuating fund currently valued at $10.8 million to protect users in case the value of their stable coin is ever threatened.

But the drawbacks of these plans is obvious: coverage is capped and not guaranteed. Both Binance and Equilibrium would be unable to recompense all of their users in the case of a significant loss, and there is no federal agency waiting to bail them out in this scenario. This means crypto users are still vulnerable to hacks and theft.

Pros of insured exchanges:

- Exchanges allow users to access their crypto with only a username and password, making exchanges far more user–friendly, simple, and convenient storage alternatives.

- Some exchanges are extremely reputable and have larger-than-average insurance funds protecting their users.

Cons of insured exchanges:

- Users do not have full control over their crypto but rather must trust the exchange to responsibly manage their funds and pay out in case of disaster.

- Unfortunately, exchanges’ insurance policies do not guarantee user funds. Whether users are refunded for their loss is at the discretion of the exchange and likely depends on the size of its liquidity pool.

- Users pay for this coverage in the form of fees. Binance hides these fees within their general exchange fees. Users pay substantially, both in terms of trading fees and withdrawal fees, to use Binance. Binance charges a 0.1% trading fee on each transaction and a withdrawal fee that can range from a fraction of a dollar to several dollars per withdrawal. Considering that coverage remains limited, users are forced to wonder whether these costs are worth it.

Insurance-backed Wallets

Some wallets, such as Civic, use the insurance provider Coincover to provide their users with insurance guarantees. Civic’s coverage guarantees user funds in case Civic goes out of business. This is known as the Coincover Deposit Guarantee.

Pros of insurance-backed wallets:

- Insurance-backed wallets do provide a certain level of protection against corporate collapse.

- They are generally free to use.

- Users stay in control of their crypto, managing their own private keys and recovery phrases.

Cons of insurance-backed wallets:

Recognize that these policies do not protect users from all losses. They only protect users if the company goes out of business. They do not protect users from a lost private key or a personal hack. These two catastrophes are the biggest threat to personally-held crypto.

Personal Wallet Insurance

For additional individual protection, crypto holders can purchase personal wallet protection, the most popular of which is Coincover’s Comprehensive Cover policy. Personal insurance guarantees crypto wallets against theft, hacks, and lost private keys.

Pros of personal crypto insurance:

- Users are protected from the most common and dangerous cryptocurrency threats.

- These options are more secure than exchange insurance offerings. Users maintain a high-level of control over their crypto (although not total control).

Cons of personal crypto insurance:

- These personal insurance plans incur high fees. Coincover’s Comprehensive Cover costs approximately .2% of the total funds every month. Compounding fees add up quickly.

- Oftentimes, this insurance applies only to a specific wallet. For example, Coincover only covers funds stored in BitGo’s multi-sig wallet. This wallet setup does not guarantee user control. Multi-sig wallets protect against private key loss by splitting up the three keys and distributing them. We previously discussed the difference between threshold signatures and multi-sig, but essentially, with this type of multi-sig, two keys are always required to make transactions. BitGo holds one key while the user holds the other two. In order to qualify for personal insurance, users must relinquish control of their second key to Coincover. This means that Coincover and BitGo collectively hold two out of the three keys required to execute transactions, and users no longer technically have control of their wallets.

- These insurance policies necessitate lots of personal information. They generally require an email, name, address, phone number, selfie images, and copies of your ID documents.

Smart Contract Insurance

Other solutions, such as Nexus Mutual and Opyn, protect against smart contract faults, such as the DAO Hack that wiped out $50 million worth of Ethereum and, in the case of Opyn, liquidity crises on behalf of centralized exchanges. These insurance options are important but less relevant for basic crypto holdings.

Pros of smart contract insurance:

Smart contract insurance can protect users from the unforeseen risks of smart contract bugs. Considering the monetary value of many smart contracts, this kind of risk-mitigation is extremely important.

Cons of smart contract insurance:

- Smart contract insurance is not free and fees scale along with the value of the contract.

- Smart contract insurance does not protect individuals from private key loss. A lost private key still locks funds in the smart contract, even if the actual contract has had no defaults.

There is no perfect crypto-insurance option

No single insurance provider protects against all faults and most focus on the situations least likely to happen. This mix and match process is not only a headache, but it racks up the fees quite quickly.

The main problem with crypto insurance offerings is that they are not fully comprehensive. For crypto holders to fully protect all of their crypto assets, they must mix and match among several different plans. They would need one plan to protect against private key loss and another for protection against smart contract faults. They might need a third to protect themselves if their wallet company ever went out of business.

Additionally, insurance companies always demand trust in a third party. Whether in the case of exchanges or personal crypto coverage, if the insurance company defaults, there will be no one to pay out on policy claims.

The reality is that there is no protection in crypto beyond the trust you have in yourself or the third-party you decide to trust. We do want to be clear that this does not mean insurance is useless, especially if it gives you peace of mind. Specifically, smart contract insurance can be very useful provided you have money secured in a smart contract.

How Does Zengo Compare?

Users are hesitant to take full responsibility for their crypto, and rightfully so. Crypto insurance gives users confidence that there’s a ‘Plan B’ if ever their crypto is lost. The question is whether it’s necessary for users to make all these sacrifices in exchange for this limited protection?

That’s why Zengo works differently, protecting you from loss and theft, but without any of the fees or the need to trust in a third-party. Removing the private key entirely is a much better solution than simply insuring against loss.

Do I need personal crypto-insurance?

Zengo works by removing the private key entirely through advanced threshold signature security, meaning that there’s never anything to lose or mismanage. All Zengo wallets rely on biometric identity and wallets can be restored on any supported device. Zengo’s unique security model means that all Zengo wallets rely on 3 separate authentication factors: the user’s email, the user’s biometric identity, and the user’s cloud account.

Lately, Zengo introduced another layer of security by providing the ability to add an additional face map. Customers can use a close family member or friend’s face to restore their wallet, thus eliminating the slight risk of losing access in case their face changes.

3FA Security ensures that with Zengo, customers don’t need an insurance policy like those offered by Binance or Coincover to protect against mismanaged keys. The protection is built right into the wallet.

Zengo is also free to use. There are no subscription fees or platform fees. Customers enjoy 24/7 support, keyless security, and full ownership with no fine print.

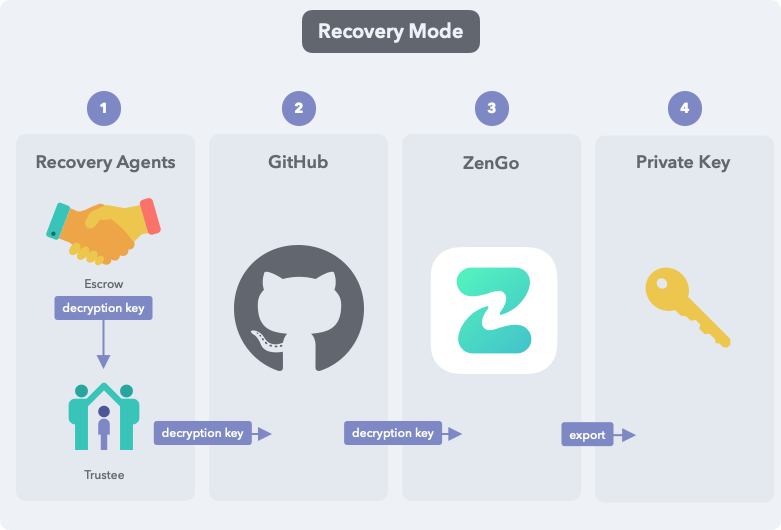

What happens if Zengo goes out of business?

Just like with many insurance guarantees, Zengo also has an Access Guarantee that protects customers should Zengo ever go out of business.

While, because of threshold signature technology, Zengo never has access to your crypto, we do store half of the secret share to make sure our customers can always restore their wallets. The Access Guarantee ensures that our customers will always have access to their crypto, no matter what.

All Zengo customers are protected under our Access Guarantee.

The Bottomline

The main challenge for crypto wallets has always been to protect users from the risks of managing their own crypto. Insurance-based wallets try to solve this with multi-sig security and guarantees against central failure. But they fail to protect against the most common risks and their form of multi-sig requires trusting central entities.

Exchanges take control of users’ funds to offer more ease and simplicity. But their insurance policies are limited and only protect a percentage of users’ funds. Full, third-party coverage is often expensive and still depends on a central entity for payouts and support.

Zengo works instead to provide systematic protection by removing the private key entirely and ensuring you full control over your crypto. And the Zengo Access Guarantee means that you don’t even need to trust Zengo.

Insurance-based wallets try to solve this with multi-sig security and guarantees against central failure. But they fail to protect against the most common risks and their form of multi-sig requires a very high level of trust in central entities.

Exchanges take control of users’ funds to offer more ease and simplicity. But their insurance policies are limited and only protect a percentage of users’ funds. Full, third-party coverage is often expensive and still depends on a central entity for payouts and support.

Zengo works instead to provide systematic protection by removing the private key entirely and ensuring you full control over your crypto. And the Zengo Access Guarantee means that you don’t even need to trust Zengo.

It’s obvious that preventing disaster is better than simply insuring against disaster. With Zengo, you get a wallet that guarantees you never lose your private key (because there isn’t one), always keeps you in control of your crypto, and ensures you never lose access to your funds.

It’s also free, because we believe that peace of mind is priceless.